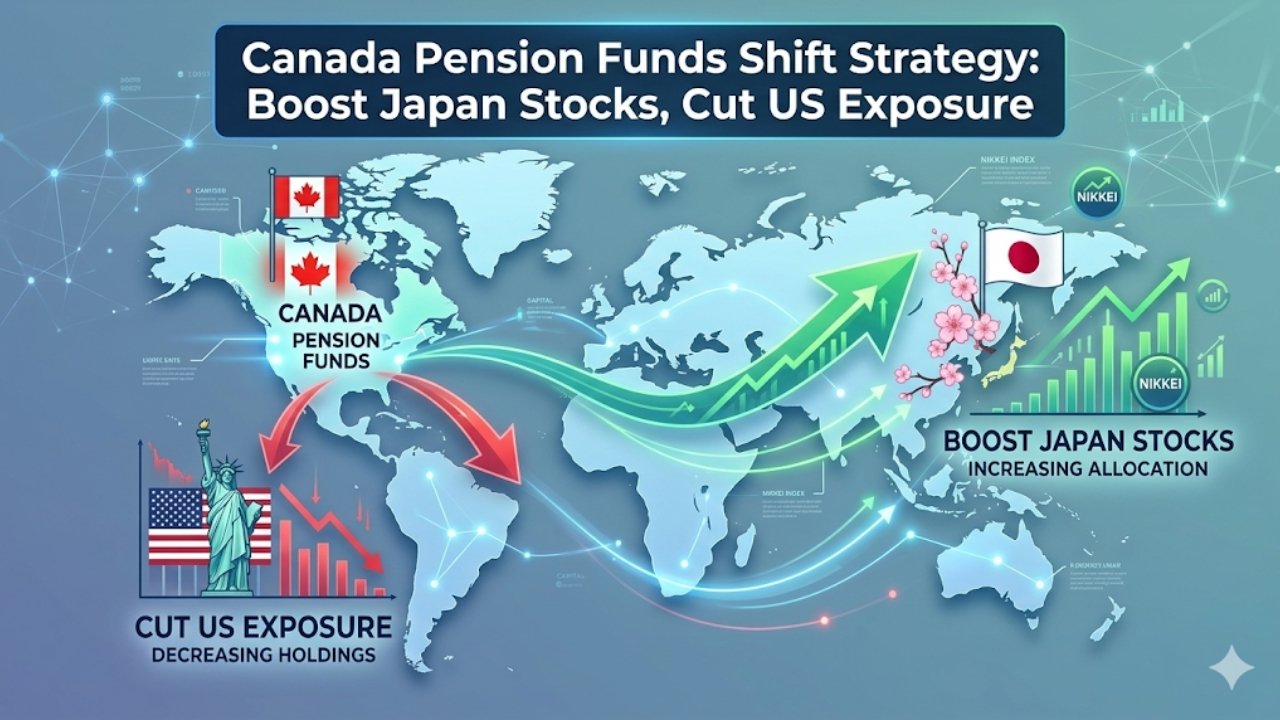

Canadian pension funds such as the Canada Pension Plan Investment Board (CPPIB) and Ontario Teachers Pension PLAN are bold in the way they are moving their portfolios. They are increasing their Japanese equities investments and reducing their investments on U.S. stocks. These changes of strategy can be noticed in their recent quarterly reports issued at the end of 2025 and in the beginning of 2026. It is indicative of a larger review of possibilities in the world market with declining U.S. market values, and the revival of Japan. These funds have a global impact since they control more than CAD 700 9 billion in combined assets under management. They are an indication of optimism in the reforms in the Japanese corporate world and the export-led development. To the simple investors who are looking back, this change highlights an important lesson that diversification is not fixed at all, but it is a pursuit of growth in value where it arises.

These patient capital, long-term, pension funds, which have perfected over decades of operating retirement savings funds on the long term, are founded on intensive internally-based research. An example of this is that CPPIB increased its investments in Japan by 15 per cent in Q4 2025. The step refers to under-priced stocks and reforms that are shareholder-friendly during the administration of Prime Ministers Fumio Kishida. In the meantime, the U.S. exposure declined around 8 percent in large funds. The tech-intensive indexes such as the S&P˙500 were trading at high price-to-earnings ratios of more than 25- perimeters of the dot-com boom days. It is not panic selling, but it is strategy rebalancing. With experience operating in the pension industry during the events such as the 2008 financial crisis and the recent 2022 inflation spike, pension managers place more value on risk-adjusted returns instead of temporary flashes.

The attractiveness of Japan is reduced to basics that have turned it to form a laggard to a leader. Since 2014, corporate Japan has been experiencing a governance overhaul. Pushes by Tokyo Stock Exchange require firms to make better on capital-efficiency–consider ¥15 trillion (approximately USD 100 billion) in share buybacks as of 2025 only. Last year, the growth in wages reached 5.3 per cent, the highest in decades, which provided domestic consumption. The small recovery of yen supports Toyota and Sony exporters. Japan has therefore come out of the deflationary trap because of inflation that has been constant at around 2.5. Stocks are more appealing and bonds less attractive. By comparison, U.S. markets are undergoing headwinds including high interest rates due to Federal Reserve tightening, political uncertainty on the 2024-2025 elections, and evidence of fatigue of earnings among the mega-cap tech companies due to AI hype challenges leveling out.

To exemplify this change in valuation between these two periods, the following snapshot of the significant metrics will be as of February 2026:

| Market/Index | P/E Ratio (Forward) | Dividend Yield | Debt-to-GDP Ratio |

|---|---|---|---|

| Nikkei 225 (Japan) | 14.2 | 2.1% | 255% |

| S&P 500 (U.S.) | 22.8 | 1.4% | 122% |

| TOPIX (Japan) | 13.9 | 2.3% | 255% |

These numbers prove the lower entry points and higher returns in Japan according to the data presented by Bloomberg and Tokyo indices. Pension funds are not putting all their eggs in one basket-Japan now makes up about 57per cent. of their equity portfolios, a 3per cent. improvement over two years ago but nevertheless it is a directional bet that fulfills their fiduciary obligation to maximize returns on Canadian retirees.

This redistribution has a ripple effect on the global investors. Having contributed to the Canadian money flowing into the market, they have contributed to pushing the Nikkei above 42,000 towards the start of 2026 to attract others such as the sovereign wealth fund of Norway, and European pensions. With the U.S. assets, the suppressed purchasing power may come to the rescue of profits particularly in the case of recession fears in case of decreasing consumer spending figures. Yet it’s not a zero‑sum game. These changes promote expanded portfolio clean. Retail investors may follow suit by looking at Japan ETFs such as the iShares MSCI Japan ETF (EWJ) that have generated returns of 18 per cent in the last one year, or indirectly through the global funds. There are always risks involved–the aging demographic of Japan and the volatility to the U.S. slowdowns should be kept up with–but the rule of thumb with the pension playbook is not to predict but to wait.

Finally, the pension stars in Canada portray a good case study of disciplined investment in an uncertain recovery period. In their preference of the reforms of Japan to the boyishness of the U.S, they are teaching us the wisdom of finding the mispricings before they become colossal. With the changing markets, such moves provide an effective guide to creating functions that are resilient portfolios.

FAQs

Q1: What is the reason why Canadian pensions are reducing U.S. stocks?

U.S. equities are not so appealing as long-term value due to high valuations and policy risks.

Q2: What is powering up the Japanese stock boom?

Corporate reforms, wage increase, and buyback have led to efficiency and investor returns.

Q3: Is this shift to be followed by individual investors?

Think about ETFs of Japan because that is going to be diversified, but first check your level of risk-taking.