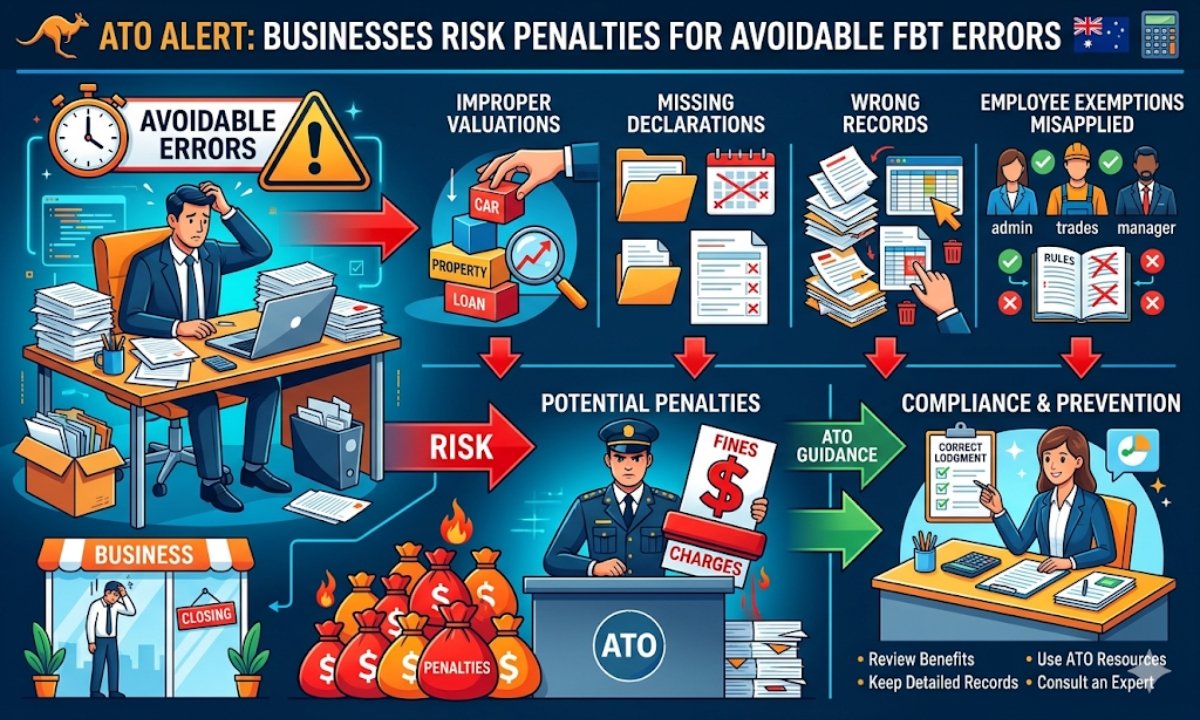

The Australian Taxation Office (ATO) is increasingly looking into Australian businesses in the area of fringe benefits tax (FBT) mistakes. Such mistakes are often brought about by the mere negligence of having in reporting the perks such as cars, meals and gym memberships of the employees. They may attract hefty fines and charge of interest as well as audit. As the tax season is nearly coming around, it is vital to know the FBT basics as well as its pitfalls in order to comply and rest peacefully.

Learning the Basics of FBT.

Fringe benefits tax is applied on the non-cash benefits offered by employers to employees including company cars that employees could use privately or subsidised housing. These are benefits and exemed by ATO as not being subject to salary or wages, and is taxed at 47 per cents of its grossed up amount in the 2025-26 FBT year that closes at 31st March. Companies are required to record and disclose such benefits in every quarter or year, and this can be done in initiative of the statutory formula used in calculating cars or the real logbook records.

A lot of small companies do not even remember that even the office workers at home may cause a FBT because of money back to home office equipment or telephone payments. Minor exemptions can be made where the benefit is less than $300 or in cases of work-benefits such as laptops and to differentiate a case, the records are to be precise. Anticipated actions anticipate unforeseen matters since the ATO has incorporated the data-matching system in identifying inconsistencies in bank calculations and superannuation accounts.

Common FBT Mistakes to Avoid

The most common mistake is to overvalue or undervalue benefits and this can be due to the fact that they do not take into consideration the percentages of the private use. Indicatively, the actual use of a between home car that is driven every day may attract FBT despite the fact that most of the use is business related but owners do not keep odometer records. It is also arguably contentious to claim meal entertainment when the client dinners are considered fully deductible without mentioning FBT regarding the same.

The liability can be reduced with the help of the employee contribution towards benefits, (e.g. they can make salary sacrifices to have a car), although they must be calculated accurately. The failure to gross -up taxable values or even to file the returns before the 21″`t May deadline attracts the automatic penalties beginning with 75 percent of the amount of tax payable in addition to interests. The latest campaigns of the ATO have been experiencing the most affected small businesses; some of which owe up to six-figure bills concerning unreported gym membership or parking allowances.

Effect of the Current Trends in ATO Enforcements.

In 225, the ATO brought on more FBT audits, with a focus on industries prevalent in perks, including hospitality and construction. Statistics indicate that there is an increase of 20-percent compliance measures, owing to AI-led investigation of the payroll information. Failure to comply is no longer only punishable but in fact now publicly blacklisted on the ATO list of tax defaulters which would be reputation-killing.

The companies which do not report on the personal tax returns on behalf of the employees only increase their problems. The change of the ATO to real-time monitoring, which is single-touch payroll, makes it more difficult to evade. Work-from-home allowances are one of the looks-over-the-nose exemptions that can be revealed online and through early contact with tax agents or ATO, due to the COVID.

| Common FBT Benefit | Typical Error | Potential Penalty Range | Avoidance Tip |

|---|---|---|---|

| Company Car | No logbook | $5,000–$50,000 | Track km monthly |

| Meal Entertainment | Double-dipping deductions | 25–75% of tax + interest | Split employee vs client costs |

| Gym Membership | Full private use ignored | $2,000–$20,000 | Apply employee contribution method |

| Phone/Internet | Reimbursements untaxed | $1,000–$10,000 | Limit to work % only |

| Parking | Near workplace overlooked | $3,000–$30,000 | Log as minor benefit if under $300/year |

.

Plans to achieve smooth FBT Conformity.

Begin by a full audit of the perks: enumerate all the benefits, approximate personal utilisation, and categorise them according to the ATO. Calculators of FBT, e.g. Xero or MYOB, are integrated, to automate gross-ups and reports. In the case of complex situations, gross-up type 2 is the option to use where there is an employee contribution relevant, which minimizes the effective rate.

Train the HR and finance departments on changes, such as the stricter policies on electric vehicle exemption which expire in 2026 when used non-commercially. Early lodging through the portal of the ATO allows avoiding glitches at peak season. Voluntary disclosures make penalties up to 80 per cent. lighter under the good faith exception in case of the errors which have been revealed.

It is credible to cooperate with registered tax advisors. I have helped more than 50 SMEs with FBT in order to transform the audit fears into reflective operations. Frequent reconciliations make sure that quarterly payments are corresponding with the real liability so that at the end of the year, there will not be any magic.

Long-term Goods of being FBT Right.

In addition to the avoidance of penalties, a good FBT management enhances cash flow through maximising exemption and contributions. Proper reporting saves thousands of dollars to firms, which they can use to grow. It also has the benefit of enhancing trust in employees, since there is no loyalty, because perk policy is transparent.

With March 2026 coming into view, act before it is late: Check the previous year and renew your policies and recalculate this year. The fewer audit comes as a reward to hard work and ATO enables more businesses to concentrate on innovation as opposed to paperwork.

FAQs

Q1: What is the FBT year‑end date?

It operates between the 1st of April and 31 st March, and returns are supposed to be made by 21 st May.

Q2: Are work laptops FBT‑free?

No, they are subject to tax unless they are mainly business based.

Q3: How can I reduce car FBT?

Actual kilometres should be used with the help of logbooks, or methods of employee contribution should be applied.