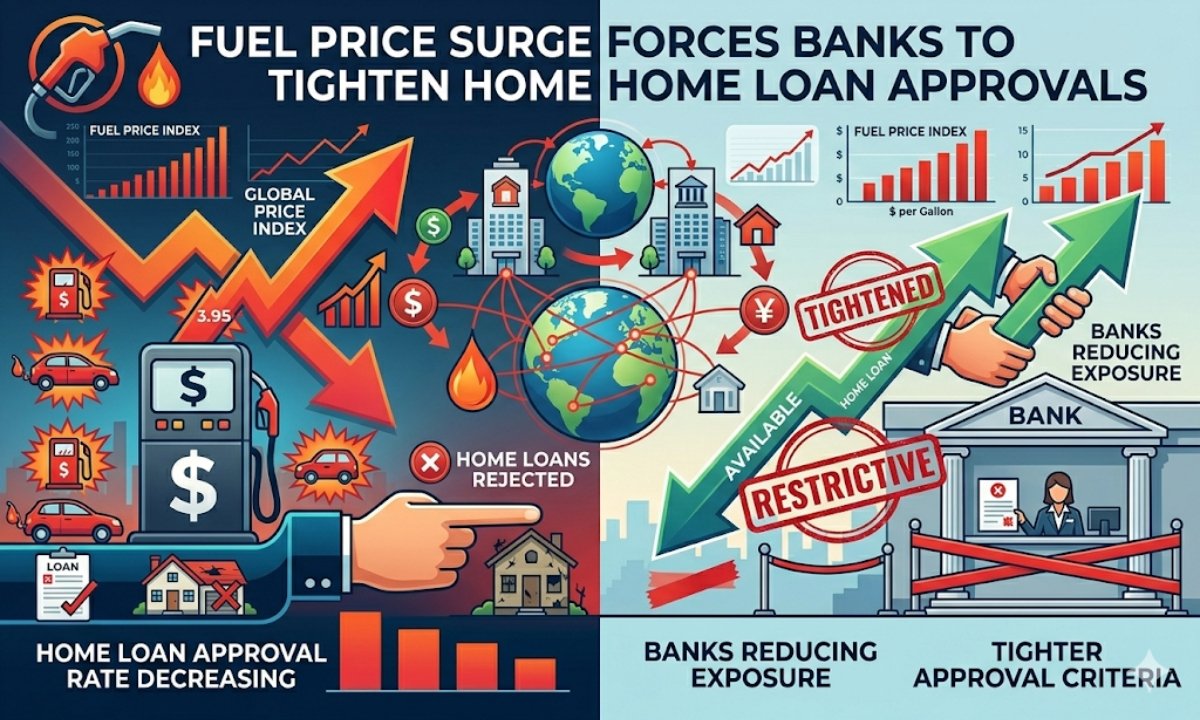

In early 2026, the Brent crude had moved above the 90 a barrel mark due to the supply reductions in Middle East, and the increased demand in the recovering economies. Increased fuel prices do not only impact on commutes. They raise inflation, weigh on household balances, and augment lender risks. In response, the banks of the U.S. and India upsurged interest rates. The outcome is the increase in the cost of borrowing. There is increased scrutiny of homebuyers and the approval rates dropped in the market to around 65 per cent of the markets where over 78 per cent were approved last year like in India and the U.S.

The lenders have raised increased down payments and perfection in credit scores. They consider the use of fuel as a threat that may cause defaults. With less disposable income, families that have to make ends meet on gasoline and diesel bills, which have already risen within India by 25 percent since January alone, are much more prone to default on mortgage payments. In 2022, the U.S. mortgage originations had been reduced by 15%. Now the banks are not heartless, they are guarding balance sheets. In India where home loans assist in urban migration, the State Bank of India secretly increased the eligibility levels. They have since given preference to salaried borrowers whose jobs were stable and not the self-employed ones who were most affected by the cost of logistics.

The effects of fuel costs on stopping inflation and putting a squeezer on borrowers.

Cars are moving, cars are running, but the entire economy is running on fuel. With increasing diesel, the cost of trucking increases and this increases the price of groceries and construction goods. India Cement prices in Q1, 2026 increased 12 per cent and the cost of new home building increased 8-10 per cent. The following inflation maintains high rates of central banks. The repo rate in India stands at 6.75 and the fed funds in the U.S stand close to 5. For buyers, this matters. A patent of 7% loan of 300,000 would cost an additional 150 to the loan of the same amount at 5.5% per month.

The impact is felt by borrowers when they are undergoing eligibility checks. Bankers are now putting their applications to trial on conditions based on fuel adjusted higher standards of living, that is, on the conditions by which the cost of petrol in question is 120L a liter. commuters and those that operate business that can run on fuel are flagged. This is detrimental to middle-class families in a place they can call home, such as Chandigarh or Mumbai, where there is little transportation available.

Bank Strategies: Between Leniency and Lockdown.

The banks have shifted to permissiveness to lockdown. They use three main defenses. First, computerized systems mark the borrowers whose fuel expenses consume a significant portion of the earnings. Second, the minimum credit scores had increased; in India, they have moved to 750 and above in order to get good rates. Third, loan-to-value ratios decreased to 75-80-percent instead of 90 percent, and thus borrowers would require additional deposit.

Take an average scenario: A Chandigarh software engineer makes ₹10 at 100000 a year. Prior to the surge, he was able to secure a 20 per cent down payment ₹60 lakh loan. Now that fuel expenses have become 15 per cent of his budget, banks restrict him to 50 lakh without presenting alternative transportation or working at home. This insures too many lenders; but retards the market. CREDAI reported that the housing sales in India had reduced by 7 percent in February 2026.

Key Impacts at a Glance

| Market | Pre-Surge Approval Rate (2025) | Current Rate (Q1 2026) | Avg. Interest Rate | Typical Down Payment Increase |

|---|---|---|---|---|

| India | 78% | 65% | 8.9% | +5-10% |

| USA | 76% | 68% | 7.2% | +8% |

| UK | 72% | 64% | 6.5% | +7% |

Prospect: Adjusting to Uncertainty.

In the future, the hope of relief does not exist soon. According to EIA, OPEC+ reductions and geopolitical tensions might continue to keep oil high until mid- 2026. The banks can relax their standards when inflation declines, but again mix of AI and human checking will still be in use. Buyers are advised to plan: select fixed-rate mortgages when you are young, create a pennant premium of fuel funds or to concentrate on efficiently consumptive houses in transit. Subsidies can be facilitated by governments. A recent ₹5,000 cr -EV push to affordable housing in India is a step in the right direction, however, it is not likely to fix anything very soon.

This surge is a wake-up call in my opinion. Fuel shock tells the extent to which housing is susceptible to energy costs. Creditors and consumers need to focus on resilience. Individuals with reduced debt, increased saving, and greener will do well.

FAQs

Q1: What has caused the fuel prices to skyrocket?

The oil has been propelled to over 90 barrels per second as a result of geopolitical tensions, reduction of the supply, and high demand following the 2025 recovery.

Q2: But what can I do to increase my chances in home loans?

Get a credit score of over 750, have at least 25 per cent down payment, and demonstrate reliable incomes even when the costs are on the increase.

Q3: Will rates drop soon?

Probably not until around the end of 2026, since central banks are struggling against current inflation due to fuel and other causes.